After years of extensive stakeholder consultation, the Australian Sustainable Finance Taxonomy is finally here. This initiative began with ASFI's release of the Australian Sustainable Finance Roadmap in 2020, which recommended the development of a sustainable finance taxonomy tailored to the Australian context.

This is also a major milestone in the Sustainable Finance Roadmap released by the Australian Government released last year, which had the taxonomy's development as priority #2, behind only mandatory climate disclosures.

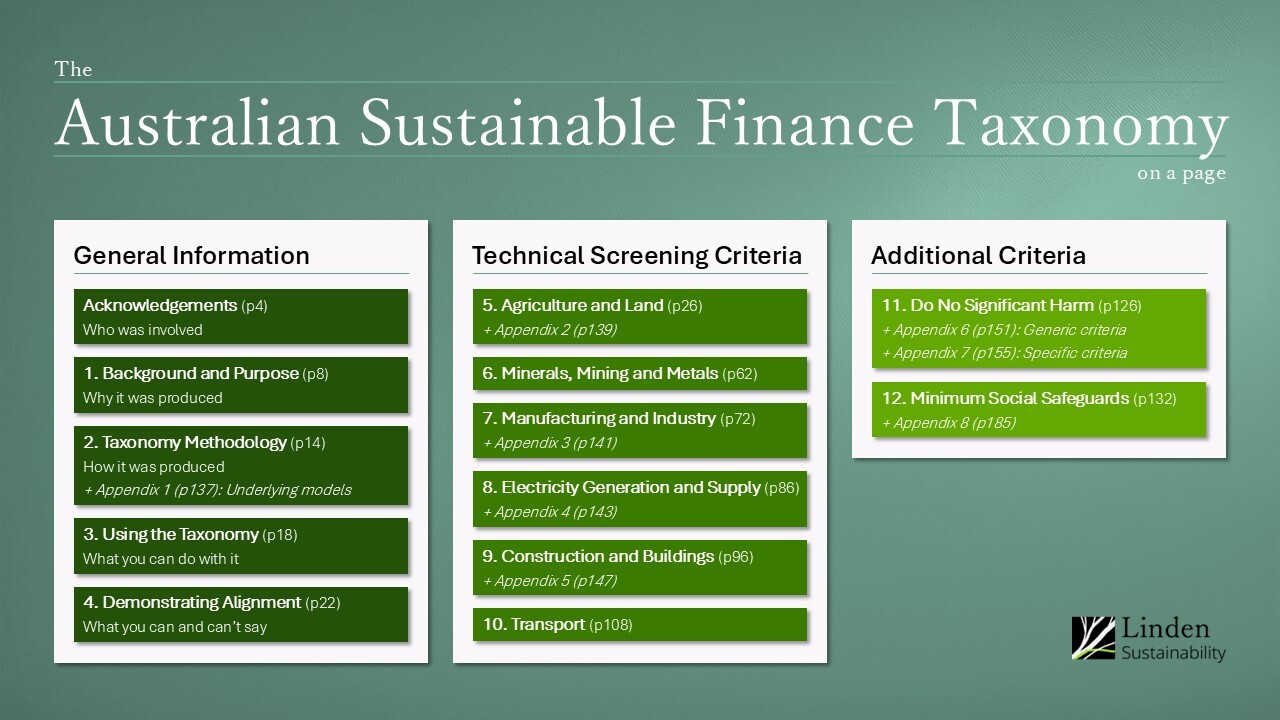

Like most taxonomies, this is a long document—198 detailed pages in total. Its twelve main sections and eight appendices can be grouped into three categories:

- Background Information on the taxonomy's development and intended use.

- The Technical Screening Criteria (TSC), forming the taxonomy's core.

- Additional Criteria, specifically Do No Significant Harm (DNSH) and Minimum Social Safeguards (MSS)

This article tackles each of those categories in turn, highlighting the major points from each core section. It doesn't intend to be a comprehensive summary, but rather a primer and guide to navigate to the sections most relevant to you.

General Information

These first four sections provide context for understanding why the taxonomy is the way it is. These sections aren't for assessing alignment with the taxonomy, despite containing frameworks that could be interpreted as such, but rather help answer questions such as why some sectors are covered and not others.

1. Background and Purpose

This section provides general information on what the taxonomy is, why it's important, and how it fits within Australia's policy landscape. It also covers how the process was governed and the guiding principles behind the taxonomy's development.

2. Taxonomy Methodology

This section explains how sectors were selected, and why some activities are classified as green while others are classified as transition.

It's worth noting that an activity's absence from the taxonomy isn't necessarily a judgement on its importance for the transition—it just didn't make it through the initial screening process. Additional sectors and activities are likely to be added over time.

Three types of activities are classified as green:

- Activities displacing emissions-intensive alternatives e.g. renewable electricity generation

- Emissions-intensive activities without green substitutes that are transitioning e.g. cement manufacturing decarbonising on a 1.5°C pathway

- Enabling activities e.g. manufacturing solar panels or installing electric vehicle charging infrastructure

The transition criteria is one of the most unique (and difficult to understand) aspects of Australia's taxonomy. It's helps to note there are two types of activities that can be assessed by the taxonomy:

- Whole activities e.g. manufacturing a product

- Decarbonisation measures e.g. energy efficiency improvements

In general, the green criteria apply to whole activities while the transition criteria apply to decarbonisation measures.

Users should first check if there are green criteria for a whole activity, and whether that activity meets the requirements. If not, that activity can't be classified as green, but specific activities to reduce emissions can still be classified as transition.

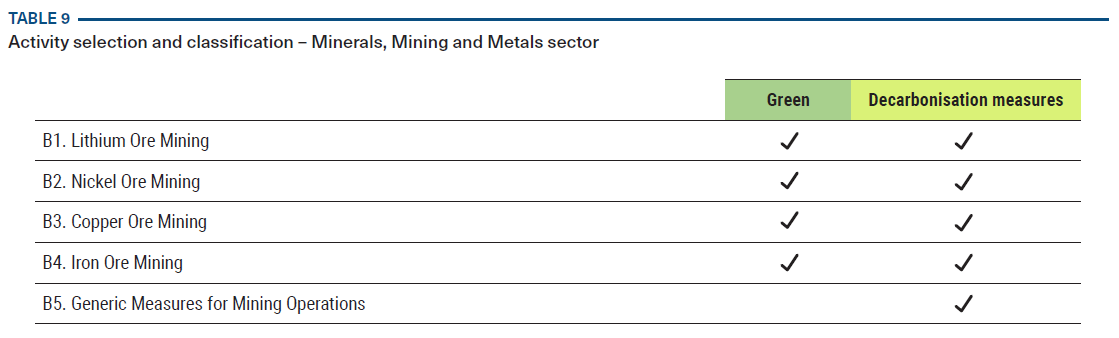

The example used by ASFI in the launch webinars was that of a lithium ore mining. There are emissions intensity thresholds (amongst other criteria) that a mine would need to hit to be classified as green. But if it doesn't meet that threshold, then the transition label can still be applied to more specific activities listed in the 'decarbonisation measures' section of the Technical Screening Criteria such as the purchase and use of low carbon liquid fuels.

There is one exception relating to classifying whole building-related activities as transition. The acquisition, ownership, renovation and upgrading of buildings that don't meet the green criteria can be labeled as transition if they meet other, less stringent criteria, but only until 1 July 2031.

3. Using the Taxonomy

This section clarifies what exactly you might do with the taxonomy, drawing on international trends and providing specific examples.

For example, the taxonomy could be used for:

- Debt instruments: Identifying eligible investments for issuing green-labelled debt.

- Corporate reporting: Voluntarily reporting taxonomy alignment.

- Transition planning: Setting alignment targets and tracking progress.

Taxonomy alignment can be assed at two levels:

- Activity: Whether an activity aligns with the taxonomy.

- Entity: The extent to which an entity’s activities align with the taxonomy e.g. the percentage of a company's revenue, capital expenditure and operational expenditure from taxonomy-aligned activities.

4. Demonstrating Taxonomy Alignment

This section provides communication guidelines around taxonomy-related claims, distinguishing three levels of alignment:

- TSC-only: Compliant with TSC but not DNSH or MSS.

- Partial: Compliant with TSC and some DNSH/MSS criteria.

- Full: Compliant with all TSC, DNSH, and MSS criteria.

The most important communication principle is transparency, particularly when it comes to what you're not aligning with e.g. none or only part of the DNSH and MSS criteria.

Crucially, this allows on-ramping of taxonomy alignment, with entities able to first assess TSC alignment, then work towards full MSS and DNHS criteria over time.

Technical Screening Criteria

The bulk of the taxonomy document is the six sector-specific sections in the middle, each structured as follows:

- Sector Context: Why the sector is important in the transition and its unique decarbonisation challenges.

- Methodology: How the activities were chosen for inclusion and how the criteria was developed.

- Technical Screening Criteria: A long list of tables clarifying the criteria for an activity to be classified as green or transition.

That last sub-section is the core of the taxonomy—the part that takes up the most room and will be used in day-to-day implementation (along with the DNSH and MSS criteria).

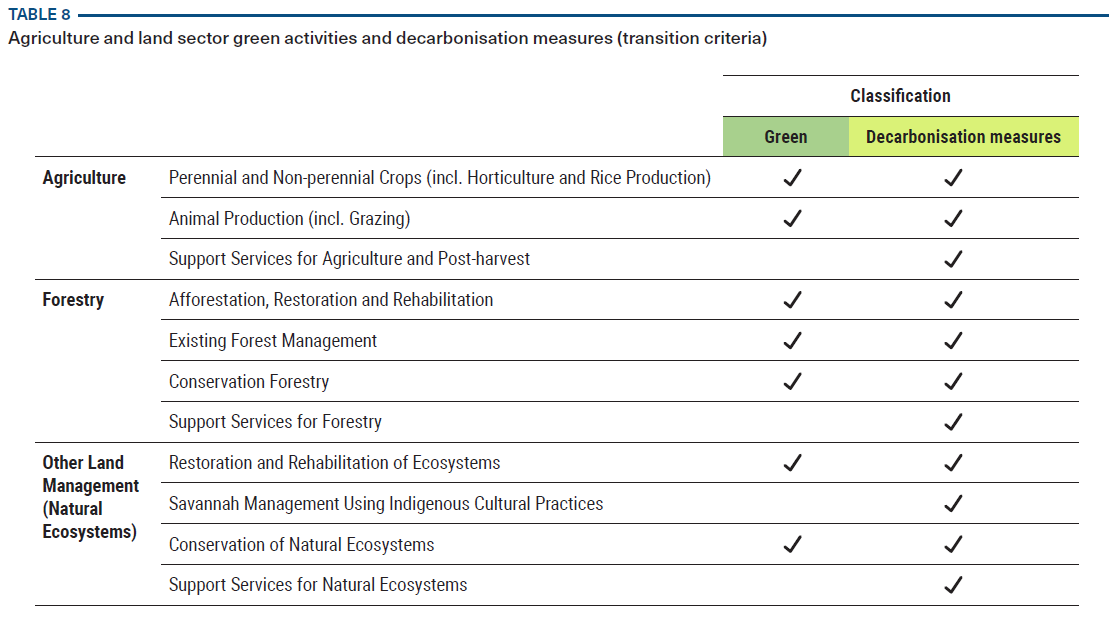

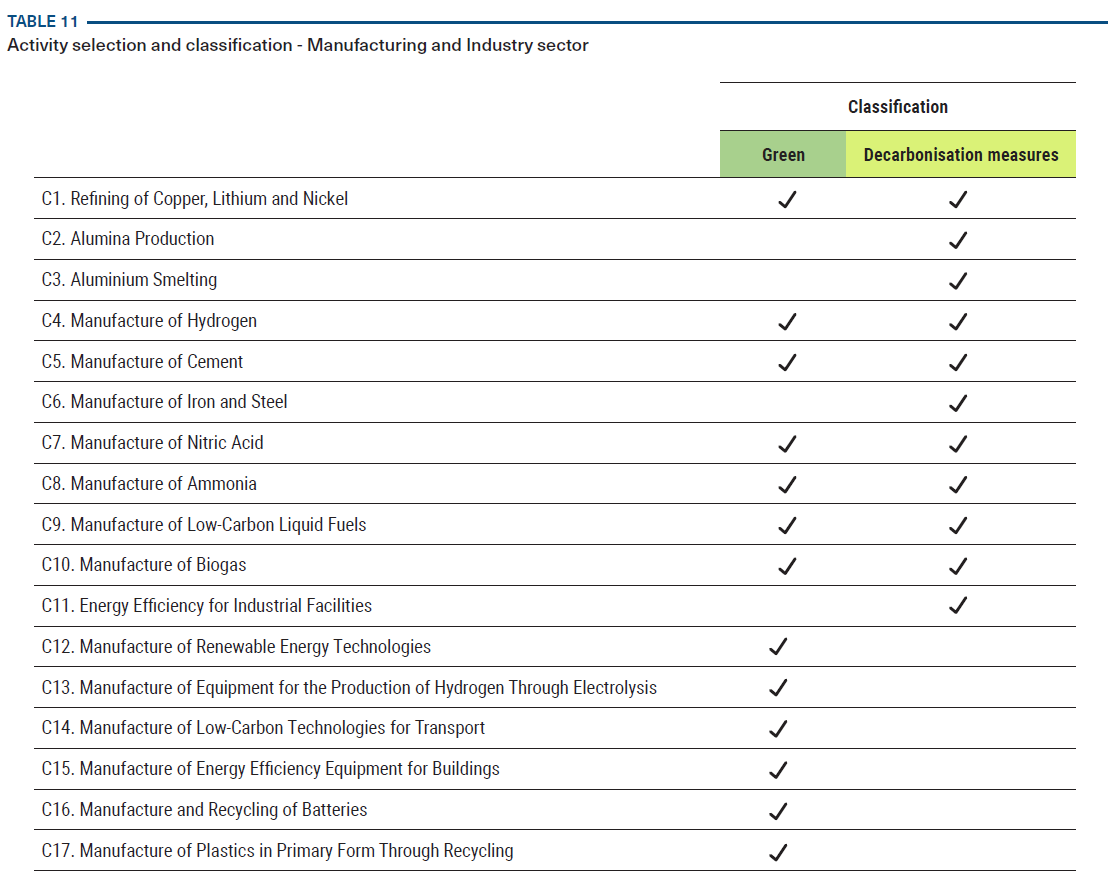

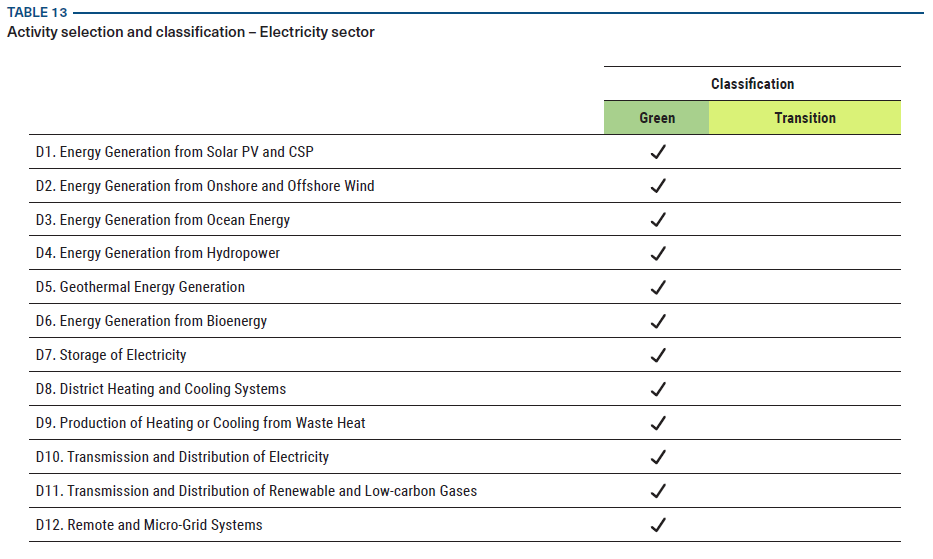

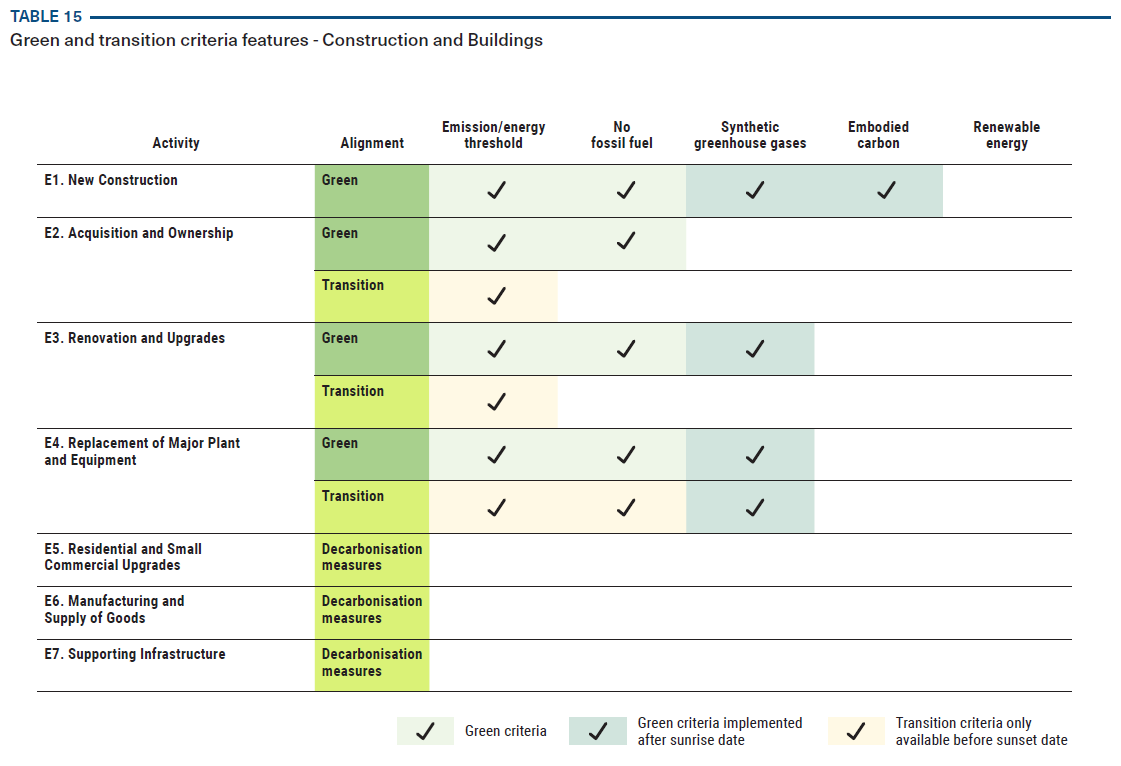

Following is the key table from each of the sector sections, summarising what activities are eligible for green or transition (decarbonisation measures) classification.

5. Agriculture and Land

6. Minerals, Mining and Metals

7. Manufacturing and Industry

8. Electricity Generation and Supply

9. Construction and Buildings

10. Transport

Additional Criteria

The last two substantive sections cover the Do No Significant Harm (DNSH) and Minimum Social Safeguards (MSS) criteria. As explained above, compliance with these additional criteria is best practice but optional, as long as the lack of alignment is clearly communicated.

11. Do No Significant Harm

There are two types of DNSH criteria:

- Generic criteria applicable to all activities.

- Specific criteria tailored to individual activities.

The generic criteria are:

- Climate change adaptation and resilience: Climate-related physical risks are identified and substantially mitigated, and the activity and adaptation solutions safeguard against maladaptation.

- Biodiversity and ecosystem protection: Biodiversity and ecosystem-related risks and impacts are identified, assessed, managed, and monitored.

- Sustainable use and protection of water resources: Water-related risks and impacts are identified, assessed, managed, and monitored.

- Pollution prevention and control: Relevant laws, regulations and standards relating to pollution are complied with.

- Circular economy: Resource use and waste are identified, minimised, and managed.

This section contains additional detail on the above generic criteria with further guidance in Appendix 6, while the specific criteria are included as a long list of tables (that line up with the TSC) in Appendix 7.

12. Minimum Social Safeguards

MSS is different from the TSC and DNSH criteria in that it applies at the entity level (e.g. the company) not the activity level.

The three pillars of the MSS criteria are:

- Corporate governance including taxation, anti-corruption and bribery, fair competition, consumer protection, and community engagement.

- Human rights including employment, labour and working conditions, occupational health and safety, modern slavery, procurement practices, gender equality, and non-discrimination and equal opportunity practices.

- First Nations including rights and cultural heritage

Specific details are provided in this section while Appendix 8 provides guidance, definitions and standards/frameworks the criteria align with.

And that's it! If you're read this far you should now have a high-level understanding of what the taxonomy is, some of the most important design features, and how to navigate the document. To learn more head here to download the full document.

Disclaimer: While I was a member of the Taxonomy Technical Expert Group (TTEG), the decision-making body for the Australian Sustainable Finance Taxonomy, any views expressed above are my own and all information shared is based on publicly available information. For official statements on the Australian Sustainable Finance Taxonomy, please contact ASFI directly.