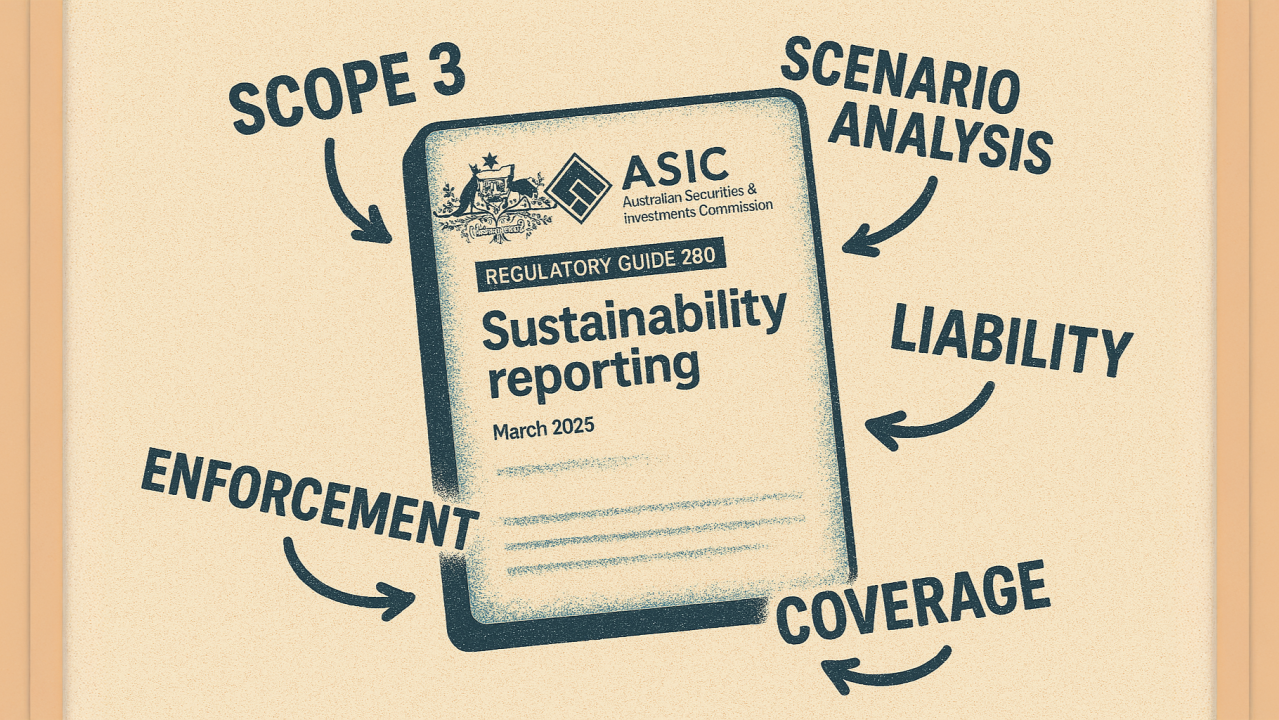

Last week, the Australian Securities and Investments Commission (ASIC) released new guidance clarifying how it will enforce mandatory climate reporting in Australia. While the guidance does not alter existing obligations under the Corporations Act and AASB S2 standards, it reduces uncertainty by outlining ASIC’s interpretation and approach. Below, we explore some key aspects of the guidance.

Coverage of Subsidiaries and Foreign Companies

ASIC has clarified several common areas of uncertainty regarding which entities must report:

- Australian subsidiaries of foreign companies must report if they independently meet the thresholds, even if the parent company publishes a consolidated sustainability report.

- Subsidiaries of Australian companies can be covered by a consolidated group report prepared by the parent company, provided the report meets all statutory requirements and appropriately includes the subsidiaries.

- Companies incorporated overseas are not required to report, even if their Australian operations meet the thresholds. However, as noted, their Australian subsidiaries must comply if they meet the criteria independently.

Governance Expectations

ASIC expects directors to take proactive steps to manage climate risk and ensure compliance. This includes:

- Establishing systems for monitoring climate risks,

- Maintaining appropriate controls for preparing sustainability disclosures, and

- Keeping accurate records.

While ASIC is clear that their guidance does not impose new obligations on directors, and taking such actions is not strictly required by the standards (only disclosure of any actions taken is generally required), the regulator sets a clear expectation for meaningful engagement with climate risk.

Scenario Analysis

ASIC reiterates that companies must consider at least two climate scenarios in their analysis: one aligned with a 1.5°C warming pathway and another representing a higher temperature outcome of 2.5°C or greater. However, it is worth noting that stakeholder expectations increasingly align with scenarios of 3°C or above.

The guidance also highlights that AASB S2 allows for proportionality in reporting, meaning companies can apply scenario analysis in a manner commensurate with their circumstances, resources, and access to reasonable and supportable information. However, due to the subjective nature of such judgements, ASIC may scrutinise the basis for these decisions and expects companies to keep adequate records to justify their approach.

Scope 3 Emissions Calculations

ASIC acknowledges the challenges companies may face in estimating Scope 3 emissions and confirms that high-level approaches—such as using spend-based emissions factors applied to financial data—are acceptable. The key expectation is that companies follow the Greenhouse Gas Protocol's guidance, with compliance and transparency taking precedence over precise accuracy in the estimates.

Liability Limitations

ASIC clarifies that protected statements generally apply only to required disclosures within the sustainability report. Voluntary disclosures or disclosures made outside the sustainability report typically fall outside these protections.

A key nuance: if a required disclosure is fulfilled by referencing another report, the referenced content is not protected under these provisions. Companies must carefully consider where and how they present key information.

Enforcement Approach

ASIC signals a balanced enforcement strategy. In most cases, it will focus on requiring corrections or improvements rather than pursuing punitive action. However, where companies are reckless in their disclosures or fail to submit a sustainability report altogether, ASIC is likely to respond more firmly. This underscores the importance of companies making genuine efforts to comply with the reporting requirements.

ASIC’s guidance provides much-needed clarity, but not complete certainty. Grey areas—such as how detailed scenario analysis should be—are unlikely to be fully resolved until the first round of reports is released and assessed.

Nonetheless, with this latest guidance, companies have most of the information they are likely to receive before reporting begins. The focus should now shift to developing robust systems and governance processes, alongside conducting the necessary analysis, to ensure companies are well-positioned to meet the reporting requirements with confidence.